Decrypting Crypto in Financial Statements: Coinbase Global, Inc (COIN)

Hey guys —

I am going to try something new here. On a recurring basis, I will be dissecting various accounting topics disclosed in public companies’ SEC filings operating in the blockchain, cryptocurrency, and Bitcoin realms. Generally, the focus will be on 10-K’s or 10-Q’s recently released to the public while diving into specific areas (i.e., revenue recognition, disclosure of crypto assets held for customers, disclosure of crypto loans, stablecoin financial statement impacts, disclosures related to regulatory guidelines, etc).

The goal is to intertwine accounting topics, current and future regulatory frameworks, and current events along with financial statement disclosures presented in public filings. We will touch on various blockchain sub-industries including but not limited to, centralized exchanges, blockchain mining companies, and crypto-adjacent companies such as PayPal, Tesla, and MicroStrategy. Today we will start with the publicly traded cryptocurrency-friendly company, Coinbase (NASDAQ: COIN), and its’ annual 10-K filing for FY2022.

Coinbase (COIN)

Coinbase Global is the “leading provider of end-to-end financial infrastructure and technology for the cryptoeconomy”1. Most of us reading this article know what Coinbase offers to the general public: a simple way to buy, sell and convert cryptocurrencies. The US cryptoeconomy falters or prospers based on the failures or successes of the company. With that said, let’s dive in.

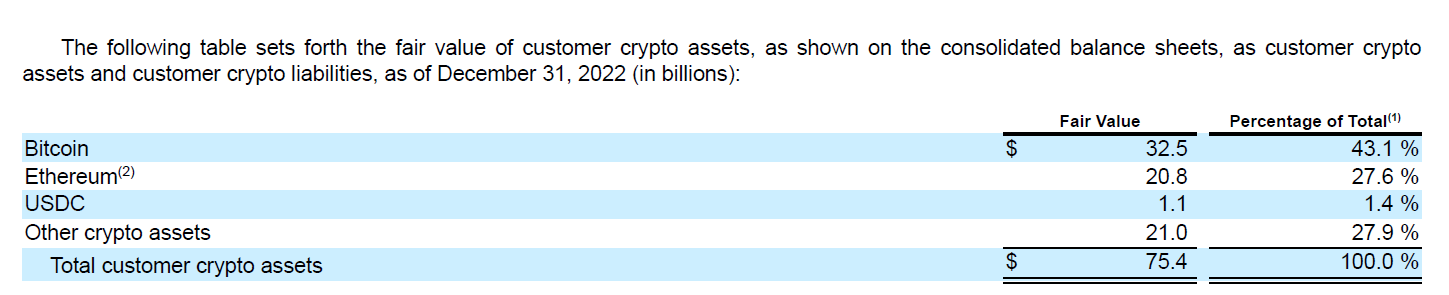

Customer Crypto Assets and Liabilities

As shown, the company’s balance sheet includes current asset/liability accounts denominated as “customer crypto assets” and “customer crypto liabilities” indicating that the company holds customers’ digital assets. This section parallels with the Staff Accounting Bulletin 121 released by the SEC (“SAB 121”), effective April 11, 2022.

The requirement stipulates that companies safeguarding customers’ crypto assets (generally applicable to centralized exchanges such as COIN) are obliged to recognize an asset for customer purchases of crypto assets and a corresponding liability. The COIN balance sheet delineates this phenomenon.

However, this requirement is subject to controversy. On one hand, 1:1 reserves of customer crypto assets held on an exchange is not preposterous. We stood by and watched FTX implode as customers of the ill-fated exchange lost millions as a result of insufficient reserves to back up customer-driven liabilities.

While COIN appears to have no issues complying, traditional financial institutions willing to immerse themselves in the industry find it difficult to abide by these rules. This is due to strict balance sheet requirements set by the banking industry based on the number of assets or liabilities held, rather than the expectation of appearing off-balance sheet. Financial institutions regulated by the government are required to maintain a % of liabilities (in reserves) to fulfill customer obligations. However, many banks would not be profitable if required to maintain these thresholds.

Some view the “problem” for traditional financial institutions as a good thing given the rehypothecation incumbent within traditional finance. Conversely, the general public likely envisions a traditional bank holding crypto assets as the safer route leading to further stagnatation of mass adoption.

The SAB 121 ruling further outlines disclosure requirements related to the risk of loss or theft. In response, Coinbase discloses the dollar amount of losses in connection with loss/theft in addition to the concentration risks associated with the crypto assets in Note 10 - see below.

Keep an eye out on the pushback of SAB 121 moving forward given the outcry from traditional finance custodians to permit off-balance sheet transactions. Additionally, with the announced crypto asset FASB updates, changes could be coming to these particular requirements.

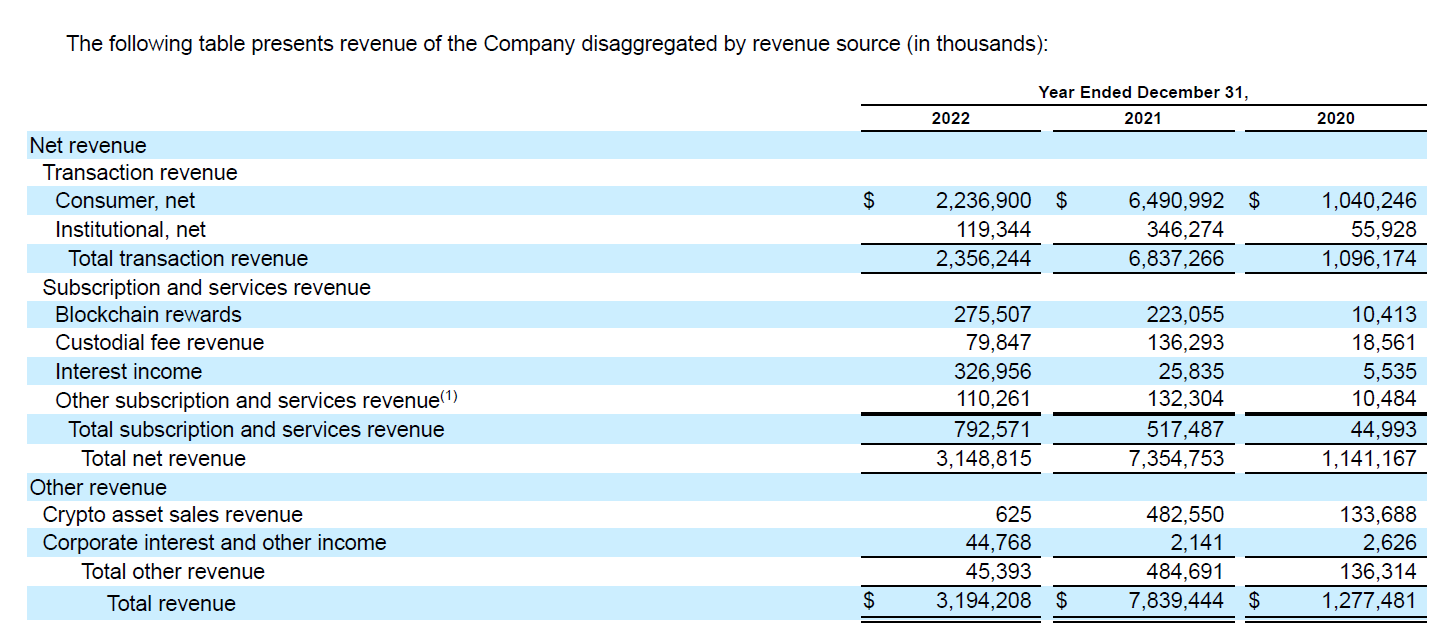

Revenue Recognition

For an exchange, the bulk of revenue recognized comes from transaction fees that are collected upon customers buying, selling or converting crypto. Coinbase delineates transaction fee revenue as “Transaction revenue” on its consolidated statement of operations.

For companies with revenue generated from transaction fees, there are a few important factors to consider when assessing revenue recognition:

Principal vs. Agent: For accounting teams, the analysis of whether the reporting entity is considered principal or agent is important. If you are operating as a principal, revenue is presented as gross revenue. Conversely, if considered an agent, revenue is present at net revenue. The Coinbase 10-K states that the company reports net transaction revenue.

“The Company evaluates the presentation of revenue on a gross or net basis based on whether it controls the crypto asset provided before it is transferred to the customer (gross) or whether it acts as an agent by arranging for other customers to provide the crypto asset to the customer (net). The Company does not control the crypto asset being provided before it is transferred to the buyer, does not have inventory risk related to the crypto asset, and is not responsible for the fulfillment of the crypto asset. The Company also does not set the price for the crypto asset as the price is a market rate established by users of the platform.”

These 3 factors contribute to the company reporting net revenue in lieu of gross revenue. Though the 10-K doesn’t specifically state the fees that reconcile gross revenue to net revenue, based on the nature of the transactions, we can assume that there are other fees involved in the transaction that COIN is required to pay, whether to validators or third parties involved in the transaction.

Variable consideration: For transactions processed, customers are known to dispute charges that occur on the platform. As such, Coinbase is required to estimate transaction fee reversals based on historical data. Once they apply an estimate (likely as a % of the total transaction revenue), a reduction in revenue gets applied to the transaction price. It is important to note that if more revenue is collected than the initial transaction price, a reassessment of the transaction price is required under ASC 606 to appropriately recognize revenue above and beyond the initial transaction price.

Material rights: For transaction fees, Coinbase does not execute a physical contract with the potential to offer customer options with a right to free or discounted goods and services. However, the company analyzes its volume-based transactional (tiered) pricing approach for a material right wherein fees are collected based on the volume of transactions executed. A material right exists when a customer obtains a discount in the future via an existing contract. In Coinbase’s case, the discount offered to the extent of the volume and materiality of the transactions chosen by its customers requires an analysis of whether a material right exists. However, because the discounting offered to its customers is parallel to what another customer could receive, no material right exists. The facts and circumstances of this conclusion will vary on a company-by-company basis.

There are many other important factors to consider in the Coinbase 10-K filing but wanted to start at a basic level to begin grasping the relevant accounting framework requirements when presenting financial statements as a company involved in the cryptocurrency realm. Stay tuned for future discussions on additional Coinbase filings in addition to my next article which will be focused on a Bitcoin mining company SEC filing.

Published in the Coinbase FY22 10-K.

I think Coinbase’s hedge accounting for cryptoassets would also be very nice to cover. Also what do you think about staking revenue accounting at Coinbase? Obviously, they act as a principal in staking business. But rewards paid to delegators should be accounted for based on the guidance on consideration payable to customers, so staking revenue should not really be grossed up...